Colorado leads the nation in hail damage insurance claims, with the Front Range averaging more billable hail days per year than almost anywhere else in the U.S. If you own a home in Denver, Aurora, Parker, or anywhere along the I-25 corridor, there's a strong chance you'll file a roof insurance claim at some point. Here's how to do it right.

Step 1: Document the Storm Date

The single most important detail in any claim is the date of loss. Insurance carriers cross-reference claims against National Weather Service hail reports. If a hailstorm hit your zip code on a specific date, your claim is far stronger when that date is on your paperwork.

Save weather alerts, take photos of accumulated hail in your yard, and write down the date and approximate time the storm hit. Even simple texts to friends ("the hail just hammered us tonight") are helpful evidence later.

Step 2: Get a Free Roof Inspection — Before Filing

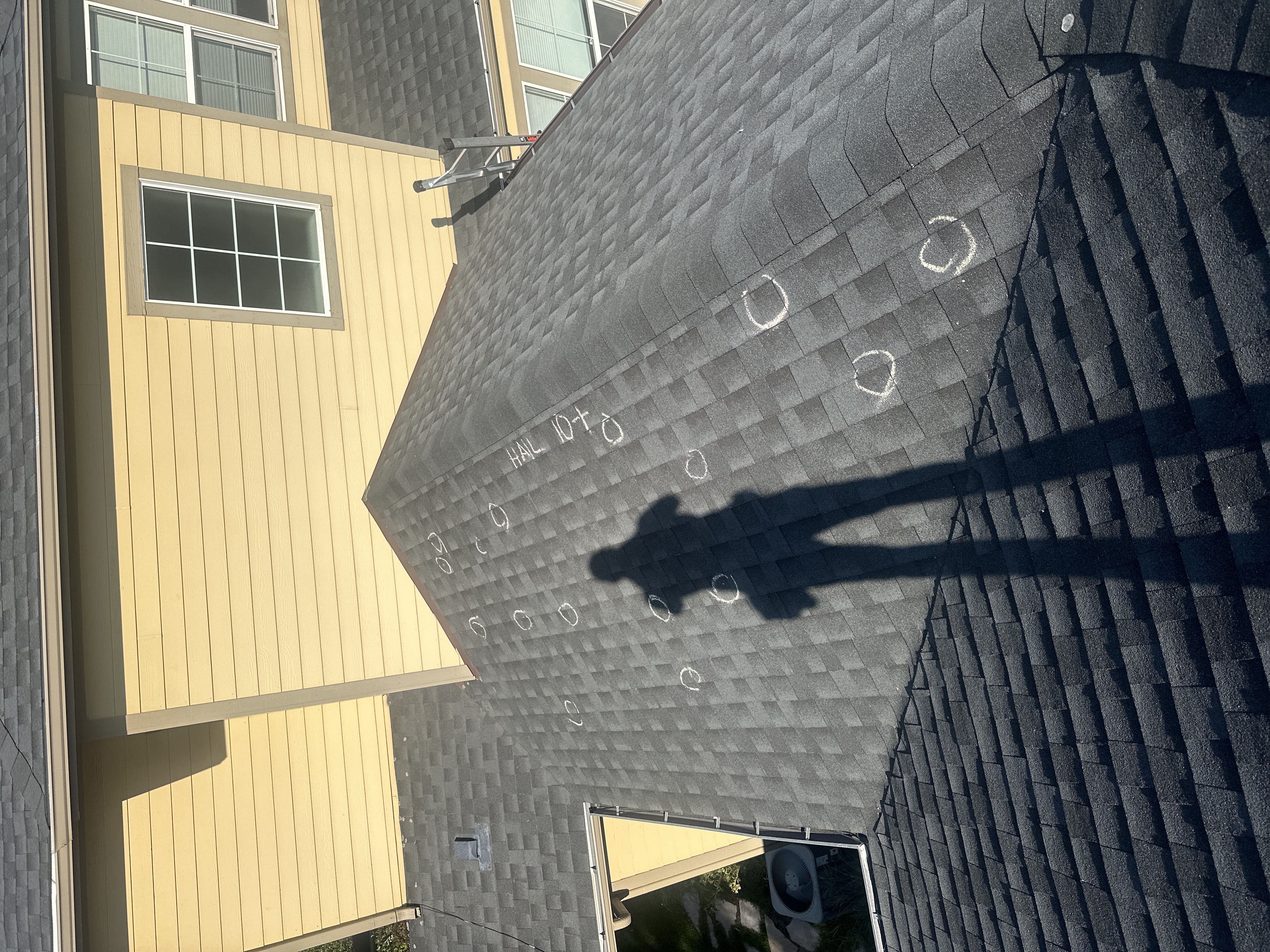

This is where most homeowners go wrong. They call their insurance company first, an adjuster comes out, finds "no functional damage," and the claim is denied. Now there's a denied claim on the homeowner's record, and any future claim faces an uphill battle.

Instead, call a reputable roofing contractor for a free inspection first. A trained roofer will climb up, photograph all damage in detail, and tell you honestly whether you have a legitimate claim. If you do, you'll go into the insurance process armed with professional documentation.

We offer free, no-obligation inspections across Denver Metro and Summit County. Whether or not we end up doing the work, you'll get an honest written report and photos of any damage we find.

Step 3: File the Claim

Once you have documentation, call your insurance company. You'll need:

- Your policy number (on your declarations page)

- The date of loss

- A description of the damage ("hail damage to roof, gutters, and siding")

- The roofing contractor's contact info if you have one

They will assign a claim number and schedule an adjuster to inspect. This typically happens within 7–14 days of filing.

Step 4: Have Your Contractor at the Adjuster Inspection

This is critical. Insurance adjusters are not your enemy, but they work for the insurance company. Their job is to write a fair scope — but "fair" often means missing items, overlooked damage, or undervalued line items.

A qualified roofing contractor at the inspection ensures every piece of damage is identified, photographed, and itemized. They speak the same technical language as the adjuster and can advocate for proper scope on your behalf.

Step 5: Review the Scope of Loss

After the inspection, your adjuster will issue a "scope of loss" document detailing what they've approved for replacement or repair. Review it carefully — and ideally, have your contractor review it too.

Common items missing from initial scopes:

- Drip edge replacement (most policies cover full replacement)

- Ice & water shield in valleys and around penetrations

- Ridge cap shingles (often underpaid)

- Detach & reset items (gutters, satellite dishes, solar)

- Code upgrades required since original installation

- Skylights, vents, and pipe boots damaged by hail

Step 6: Negotiate Supplements If Needed

If your contractor finds items missing from the scope, they can submit a "supplement" — a request for additional payment from the insurance company with documentation. This is a normal, expected part of the process. Carriers reserve funds specifically for supplements.

Step 7: Sign the Contract and Schedule Installation

Once the scope is finalized, you sign a contract with your roofer for the agreed-upon amount. Your insurance pays the contractor (minus your deductible, which is your only out-of-pocket cost) and the work gets scheduled.

You are NOT obligated to use a specific contractor your insurance recommends. You have the right to choose any licensed, insured roofer in Colorado. Carriers may suggest their "preferred" contractors, but they cannot require it.

What to Avoid

- Door-to-door "storm chasers." Out-of-state contractors who show up after a storm, take your deposit, and disappear. Always verify Colorado licensing and local references.

- Anyone offering to "eat your deductible." This is insurance fraud — illegal in Colorado, and it can void your policy.

- Waiting too long. Colorado law generally requires storm damage claims to be filed within 1 year of date of loss.

- Signing anything before you understand it. Get written estimates, read contracts, and ask questions.

How Long Does the Whole Process Take?

A typical Colorado roof insurance claim, from first call to installed roof, runs 30–60 days. Major hail seasons can extend that timeline as adjusters and contractors get backed up. The actual roof installation itself is usually just 1–2 days.

When You Need Help

Filing your first storm damage claim can feel overwhelming. At Force 5 Roofing, we walk Denver Metro and Summit County homeowners through this process every week. We handle the documentation, attend the adjuster inspection, file supplements when needed, and install the new roof — all coordinated as one process.